Hidden in Plain Sight: How Insurer Middlemen Pocket the Savings Meant to Lower Patient Costs

- May 13

- 3 min read

Each year, premiums go up, deductibles increase, and insurers and their affiliated PBMs make record profits. In recent years, investigations and hearings have been uncovering how this happens.

During a 2025 congressional hearing on PBM practices, Witness Dr. Hugh Chancy, a Georgia pharmacist and former president of the National Community Pharmacists Association, described a story of a customer whose prescription cost $135 at the pharmacy – yet their insurance plan was billed $400 by the PBM. When they questioned it, they were told the plan simply paid $400. The difference went straight to the PBM - not to the doctor, not to the pharmacy and certainly not back to the patient.

That gap is spread pricing. And it is happening on prescriptions across the country, every day.

What Is Spread Pricing ?

When an employer or insurer hires a PBM to manage prescription drug benefits, the PBM negotiates prices with pharmacies and in theory, those savings pass through to patients. In practice, the PBM can charge an employer or health plan significantly more for a drug than it actually pays the pharmacy to dispense it and keep the difference. The spread is hidden. The markup is hidden. And for years, there was no requirement that this be disclosed.

According to the Federal Trade Commission (FTC), the three largest PBMs brought in $1.4 billion from spread pricing between 2017 and 2021 alone. That is $1.4 billion that should have stayed with employers, patients and taxpayers – instead absorbed quietly into the bottom line of the large corporations.

More Markups In the Shadows

Spread pricing is only one piece of the puzzle. The FTC’s landmark investigation into the Big Three PBMs exposed a broader pattern of hidden markups that goes well beyond the spread.

Between 2017 and 2022, PBM-affiliated pharmacies generated more than $7.3 billion in revenue above the estimated acquisition cost of specialty generic drugs – treatments for cancer, HIV and other serious conditions. In one example, PBMs marked up tadalafil, a pulmonary hypertension medication, by 7,736% for commercial payers in 2022.

Meanwhile, 42 cents of every dollar spent on brand-name drugs now goes to PBMs in the form of rebates and fees. Those rebates were supposed to lower patient costs.

One Corporation, Every Role

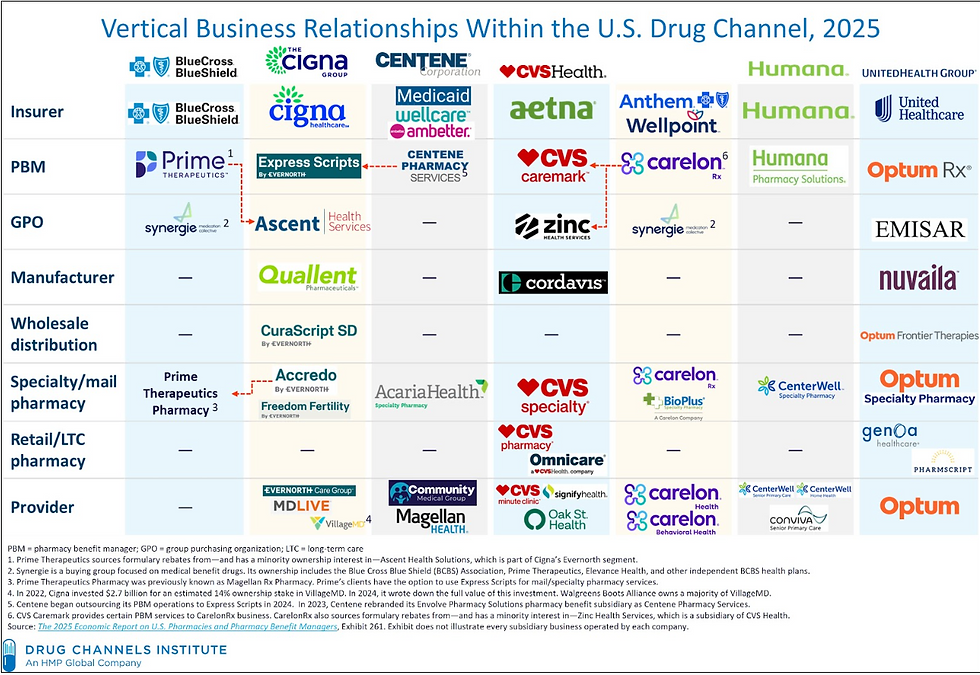

This is not simply a story about pricing tricks. It is a story about what happens when the same corporation controls every lever in the system.

Nearly 80% of all U.S. prescription drug claims are controlled by just three PBMs, vertically integrated with insurance companies and pharmacies. When the insurer, the PBM, and the pharmacy all answer to the same parent company, the incentive to pass savings along to patients disappears. Every dollar captured stays inside the conglomerate – recaptured from the very employers and patients the system is supposed to serve.

The Reform Moment

PBM-related reforms are projected to save the federal government nearly $5 billion through fairer pharmacy reimbursement, eliminating secret rebate deals, requiring pricing transparency and ending hidden fees. But those savings only materialize if the structural conflicts of interest driving the problem are addressed alongside the pricing rules.

As long as the same corporation controls the insurance plan, the PBM and the pharmacy, it will find new ways to recapture what reform tries to return. Transparency without structural accountability is a press release, not a fix.

Learn more about policy solutions here.